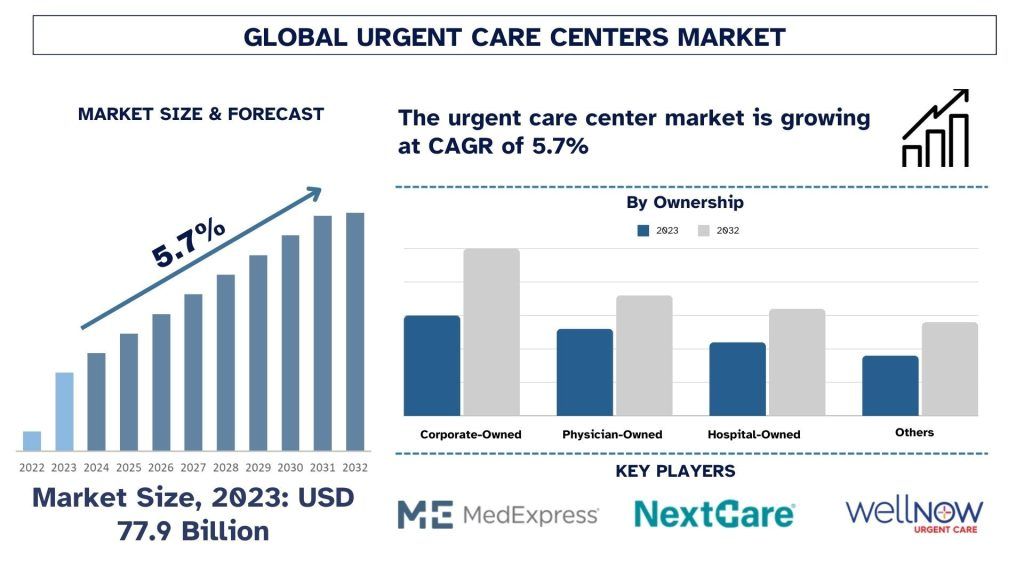

According to UnivDatos, the Urgent Care Centers Market was valued at approximately USD 77.9 billion in 2023 and is projected to expand at a strong CAGR of about 5.7% during the forecast period (2024–2032). This growth is primarily driven by the rising demand for convenient and cost-effective healthcare services, coupled with a shortage of primary care physicians and persistent overcrowding in hospital emergency departments. Furthermore, the growing adoption of telemedicine and the increasing need for rapid, easily accessible treatment for non-life-threatening medical conditions are further accelerating market expansion.

An urgent care center (UCC)—also referred to as an urgent treatment center—is a walk-in medical facility designed to deliver immediate care for non-emergency health issues. These centers serve as an effective alternative to hospital emergency rooms by providing timely treatment for conditions that require prompt attention but do not necessitate emergency-level resources. By offering accessible, efficient, and affordable outpatient services, urgent care centers effectively bridge the gap between primary care practices and emergency departments.

Access sample report (including graphs, charts, and figures): https://univdatos.com/reports/urgent-care-centers-market?popup=report-enquiry

Urgent care centers address a broad spectrum of medical conditions, including minor fractures, sprains, lacerations requiring stitches, burns, infections, respiratory ailments, dermatological issues, and gastrointestinal disorders. They are also commonly used for treating sports-related injuries, back pain, allergic reactions, and seasonal illnesses such as influenza and colds. The rising incidence of these conditions has significantly increased the demand for urgent care services. In particular, injuries associated with sports and recreational activities, including those involving exercise equipment, represent a substantial portion of urgent care visits, highlighting the importance of readily accessible treatment facilities.

The global urgent care centers market is witnessing consistent growth, largely supported by the expanding insured population and greater awareness of alternative healthcare options outside traditional hospital environments. With improved insurance coverage, patients are increasingly opting for urgent care centers instead of delaying treatment or relying solely on emergency departments. Factors such as shorter wait times, extended hours of operation, and lower treatment costs compared to emergency rooms continue to make urgent care centers an appealing choice for both patients and payers.

To strengthen their market position, leading players are adopting various strategic initiatives, including the launch of new urgent care brands, expansion of clinic networks, and the implementation of patient-focused care models. These strategies emphasize affordability, convenience, and personalized care, helping organizations enhance patient satisfaction while meeting the growing need for immediate medical services across both urban and suburban regions.

Based on medical services, the urgent care centers market is segmented into acute illness treatment, trauma and injury treatment, physical examinations, immunizations and vaccinations, and other healthcare services. Among these, trauma and injury treatment is expected to register significant growth during the forecast period. This trend is driven by the increasing occurrence of minor and major injuries resulting from accidents, physical activities, and workplace hazards. A large proportion of individuals experience at least one traumatic incident during their lifetime, and urgent care centers play a vital role in providing rapid assessment and treatment. Men, in particular, show a higher likelihood of trauma exposure due to accidents, violence, combat, disasters, or witnessing severe injuries, which further boosts demand for trauma-related urgent care services.

In terms of ownership structure, the market is categorized into corporate-owned, physician-owned, hospital-owned, and other models. Corporate-owned urgent care centers account for a significant share of the market, supported by robust investments from private equity firms, insurance providers, and large healthcare organizations. These operators benefit from economies of scale, enabling them to streamline operations and reduce costs. By employing nurse practitioners and medical assistants, negotiating favorable supplier contracts, and outsourcing administrative and technological services, corporate-owned centers deliver standardized, high-quality care across multiple locations at competitive prices.

Physician-owned urgent care centers, although smaller in scale, remain essential in many communities, particularly where personalized, physician-led care is highly valued. Meanwhile, hospital-owned urgent care centers are gaining momentum as healthcare systems aim to expand outpatient services and alleviate pressure on emergency departments. These centers allow hospitals to better manage patient flow while extending their brand presence into community-based care settings.

From a regional standpoint, the urgent care centers market is evaluated across North America, Europe, Asia-Pacific, and the rest of the world. North America represents a mature market, supported by advanced healthcare infrastructure, high insurance penetration, and widespread utilization of urgent care services. Europe is also experiencing steady growth, driven by rising healthcare investments and increasing acceptance of walk-in care models.

Click here to view the Report Description & TOC: https://univdatos.com/reports/urgent-care-centers-market

The Asia-Pacific region is expected to witness the fastest growth during the forecast period. Key growth drivers include increasing healthcare expenditure, greater awareness of urgent medical services, and rising demand for emergency and ambulatory care facilities. Additionally, the region’s rapidly growing aging population is more prone to chronic illnesses, injuries, and acute conditions requiring immediate care. Ongoing improvements in healthcare infrastructure and supportive government initiatives are further accelerating the adoption of urgent care centers across several Asia-Pacific countries.

Healthcare spending in emerging Asia-Pacific economies continues to rise, reflecting a stronger emphasis on improving healthcare accessibility and outcomes. With increasing disposable incomes and rapid urbanization, consumers are seeking convenient and flexible healthcare solutions that align with modern lifestyles. Urgent care centers, offering extended hours and a wide range of services, are well-positioned to meet these evolving demands.

The global urgent care centers market features the presence of several key industry players that are actively expanding their service offerings and geographic footprint. Major companies operating in this market include Concentra, Inc., MedExpress, NextCare, TH Medical, FastMed Urgent Care, Ascension, Summit Health, WellNow Urgent Care, American Family Care, and GoHealth Urgent Care. These organizations are focusing on strategic partnerships, acquisitions, and service innovation to enhance their competitive positioning and address the rising global demand for urgent medical care.

In summary, the urgent care centers market is set for continued and sustainable growth as healthcare systems worldwide increasingly prioritize efficiency, accessibility, and patient-centric care. The growing prevalence of injuries, acute illnesses, and lifestyle-related health conditions—along with the need to reduce emergency department congestion—continues to drive the widespread adoption of urgent care centers across both developed and developing regions.

Contact Us:

UnivDatos

Contact Number – +1 978 733 0253

Email – contact@univdatos.com

Website – www.univdatos.com

Linkedin- https://www.linkedin.com/company/univ-datos-market-insight/mycompany/